As countries around the world strive to achieve net zero emissions, the wave of sustainable development continues to impact various fields, followed by huge investment opportunities hidden under the theme of potential.

In the past few years, the rising global temperature and the frequent occurrence of extreme climates have continued to impact the social and economic development of human beings. The net zero target of the Paris Agreement points out the direction for the world to jointly address climate change. However, according to the 2021 Emissions Gap Report released by the United Nations Environment Programme, it is estimated based on the current emission status of countries and their reported climate change mitigation commitments. There is still a big gap between the target of an increase of less than 1.5°C.

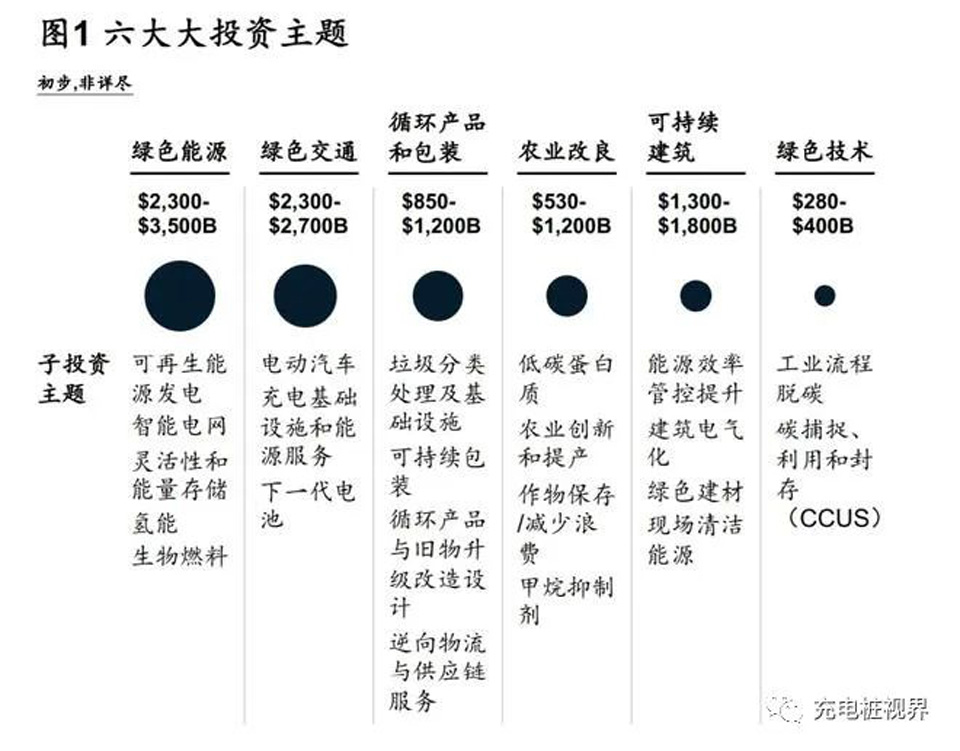

To achieve the net zero goal, global policy mechanisms, technological innovation, and consumer awareness will continue to improve, and more sustainable investment opportunities will emerge. Focusing on the mitigation and adaptation of climate risks, after comprehensive consideration of investment feasibility and development potential, we have summarized six investment themes (see Figure 1). By 2030, these themes are expected to generate a combined investment opportunity of approximately $7 trillion to $11 trillion.

In the past few years, these six investment themes have been widely favored by investors, especially the sub-segments such as new energy and electric vehicles, which are also hot spots for capital chasing. A number of industry giants with high market capitalization have emerged at home and abroad.

However, this is just the beginning. Based on our observation and analysis, from the perspective of the whole industry chain, other sub-track industries and companies under these six investment themes are also accelerating their growth, bringing huge potential investment opportunities. This article will focus on analyzing the six major investment themes and their core subdivisions, and in the process of digging deep into the track, focus on discussing the next round of potential growth points.

Investment Theme Size Estimation Instructions

Our market potential estimates are mainly based on the following core assumptions, and the actual market potential may be greater.

- The industry will continue the current trend in the application of past technologies or new technologies, and there will be no major unexpected changes;

- Continuation of existing trends in consumer behaviour, adjusted for possible impacts of climate change;

- There will be no significant unanticipated intervention in the market by regulation (i.e. there will be no significant impact).

The size estimates for each investment thesis are based on a combination of technological changes, changes in consumer preferences, regulatory and macroeconomic factors. In addition, each market size estimate takes into account the certainty of that valuation, i.e. some investment opportunities have high certainty and some investment opportunities have low certainty.

This article will introduce the green energy and green transportation that you are more concerned about

01 Green Energy

The energy industry is the world's largest emitter of greenhouse gases. In China, CO2 emissions from fuel combustion and industrial production exceeded 11 Gt in 2020, and coal-fired power stations alone (including cogeneration plants) accounted for more than 45% of China’s overall energy consumption and production-related emissions, accounting for global 15% of emissions. It can be seen that decarbonizing the energy industry and realizing the transition from fossil energy to green energy are the keys to achieving the global net zero goal.

The transition to green energy has created significant investment needs. Taking the decarbonization of the power industry as an example, it is first necessary to use investment to transform power generation energy from fossil energy to clean energy such as renewable energy, and to strengthen the existing system so that it can better withstand the effects of climate change. Among them, when deploying clean energy, a large amount of infrastructure is required, which in turn generates additional investment requirements. In addition, achieving 100% decarbonization of the power sector will require a host of tools, including new technologies, cheap and flexible grid systems to manage intermittent (and often distributed) generation, and more. In addition, as the climate warms, extreme weather phenomena such as forest fires, hurricanes, floods, etc. are frequently raging. Strengthening and improving the resilience of power grids has become a must and an important sustainable investment direction.

We predict that by 2030, the green energy sector will generate about $2.3 trillion to $3.5 trillion in investment opportunities, including renewable energy generation, smart grids, power system flexibility and energy storage solutions, grid and customer energy analysis, hydrogen energy , biofuels and other sub-tracks have great potential and are worthy of focus.

In recent years, renewable energy projects including hydropower, solar power, nuclear power and wind power have continued to increase and are expected to become the largest potential investment track. In terms of cost, the cost of renewable energy has been declining in recent years, which can compete with the price of traditional fossil energy, and the growth rate of demand scale continues to soar. At the same time, the cost of energy storage continues to decline, further increasing the penetration of renewable energy sources to displace coal and gas. In terms of policies, many countries and regions have announced clean energy targets (for example, the European Union is committed to achieving 20% of total energy consumption by 2020 from renewable energy), and formulated corresponding policies to encourage the energy industry to switch to green energy ( Such as feed-in tariff subsidies, tax incentives, etc.), further promoting the development of renewable energy. In addition, the current profitability of renewable energy power generation is relatively weak, and it is highly dependent on government subsidies. It is necessary to further strengthen technology research and development and investment to optimize costs.

Smart grid is the key investment direction of the national grid construction, and the investment scale is increasing year by year. According to the State Grid Intelligent Planning General Report issued by the State Grid, in the three construction stages of "Strong Smart Grid", the proportion of smart grid investment in the total grid investment is 6.19%, 11.67%, and 12.50%, respectively, showing a continuous trend. Upward trend. Mao Weiming, chairman of State Grid, estimated that during the "14th Five-Year Plan" period, the total investment in power grids and related industries will exceed 6 trillion yuan. In addition, driven by carbon neutral policies, smart grids can also become an important strategic measure for the country to promote a low-carbon economy by promoting the organic integration of energy and the Internet.

At the same time, with falling costs and expanding demand for new energy sources, the power system flexibility and energy storage markets are also growing rapidly to deal with energy storage problems and huge storage issues brought about by the cyclical nature of renewable energy (such as the inability of solar energy to be produced at night). capacity requirements. In recent years, European and American countries have developed vigorously in the field of energy storage, and China has also strengthened its attention and layout of the energy storage industry. In July 2021, the National Development and Reform Commission and the National Energy Administration jointly issued the "Guiding Opinions on Accelerating the Development of New Energy Storage", proposing that "by 2030, the comprehensive market-oriented development of new energy storage will be realized, and new energy storage will become the carbon peak in the energy field. one of the key underpinnings of carbon neutrality”. Some leading companies have also accelerated the deployment of energy storage. For example, a leading domestic new energy technology company and a large state-owned investment group invested tens of millions of yuan to establish an energy storage development company to fully promote the investment, construction and operation of energy storage projects.

In addition, low-carbon fuels (including hydrogen and bioenergy) will also play a key role in the decarbonization process, achieving further emission reductions based on the existing energy combustion system. Based on our estimates, hydrogen energy could meet about 5% of renewable electricity demand by 2030 under a scenario of global warming and temperature rise limited to 2°C, with an annual market revenue of over $200 billion. In addition, some countries and regions are also promoting the development of hydrogen energy. For example, the European Union announced the "Green Hydrogen Energy Strategy" in 2020, and plans to increase investment in the hydrogen energy industry in the next 10 years.

Biofuels mainly come from various animal and vegetable oils and fats. They have become a weapon for reducing emissions because they can almost achieve carbon neutrality, and have attracted the attention of various countries. The EU's Renewable Energy Directive implemented in 2009 stipulates that the blending ratio of biofuels in the transportation sector should reach 10% by 2020. Biofuels mainly include second-generation biodiesel (HVO/HEFA) fuels, waste fuels (through pyrolysis or gasification processes), and electric fuels. Among them, the development speed of biofuels in Europe is higher than that of the United States, and the investment potential is huge. From an investment perspective, investors can focus on the three major directions of large-scale production of biofuels through biomass, conversion of waste into fuels through pyrolysis processes, and gasification of waste fuels.

Track Digging - Smart Grid

Smart grid is the integration of traditional power grid with a variety of new technologies, new equipment, and new materials, including two directions of grid modernization and flexible grid. Grid modernization is a process in which operators use digital and intelligent technologies to monitor power flow and consumption in order to respond to user needs in a more timely manner. With the reduction of technology costs and the continuous advancement of digitalization, power grid modernization is increasingly favored by investors, and various companies have begun to deploy software and hardware support and maintenance services. A resilient power grid refers to a power grid that can respond to low-probability and high-risk extreme events in a timely manner, minimize the impact of events, and have the ability to quickly restore power supply. In recent years, the frequency of extreme weather has increased and the associated maintenance costs have been high, which have all contributed to the development of this field. Power companies hope to improve efficiency and reduce costs through a modern and resilient grid, so a group of companies focusing on providing software and hardware support and maintenance services have emerged.

With the expansion of the scale of the national power grid and the increase in the complexity of the lines, the construction of smart grids has gradually been listed as a key strategy in China. For example, the construction of smart grids in 2021 was included in the "14th Five-Year Plan", which mentioned that the intelligent transformation of power grid infrastructure and the construction of smart microgrids should be accelerated to improve the complementary and intelligent adjustment capabilities of the power system.

In addition to state-owned power companies, start-ups are also emerging in the smart grid. For example, in 2021, a domestic start-up company received tens of millions of yuan in Series A financing, and its distributed energy storage system can give full play to the function of a virtual power plant during the peak load time period of the regional power grid, quell the superimposed peak load demand in the region, and delay large-scale Supply-side infrastructure construction and transmission network and distribution network construction, thereby improving the asset rate of the power generation side and the transmission side and saving investment costs. In addition, according to the needs of underdeveloped areas with weak power infrastructure, the company has launched a micro-grid system to gradually replace traditional diesel generator sets. Demand, help users solve the energy consumption in daily life, and open a new chapter in green energy consumption.

Another start-up company provides AI solutions for power grid inspection based on visual recognition, and is committed to solving the problems of difficult circuit inspection and complex operation and maintenance work. Due to the large scale of the power grid, the traditional manual inspection has a large workload and high operation and maintenance costs, and because the power grid is mostly located in remote mountainous areas, there are many safety problems and hidden dangers in the inspection. The company provides integrated software and hardware solutions from algorithms, software platforms, data analysis, intelligent detection equipment to intelligent terminals, which can realize AI monitoring of transmission line defects, intelligent protection against external breaches, intelligent analysis of power personnel behavior, and intelligent safety supervision of power grids and other functions. At present, the company has received Pre-A round of financing.

Track Deep Excavation - Hydrogen Energy

About 30% of global carbon dioxide emissions are related to energy consumption. It is difficult to achieve comprehensive emission reduction only by improving smart grids, and it is necessary to switch to low-carbon fuels. In the next 1-3 years, one of the three main low-carbon fuels worth considering for investment is hydrogen energy. Based on our estimates, hydrogen energy could meet about 5% of renewable electricity demand by 2030 under a scenario of global warming and a temperature rise of less than 2°C, with annual market revenue expected to exceed $200 billion.

Meanwhile, hydrogen energy is expected to play a vital role in China's decarbonization pathway. With the reduction of electricity costs and the development of hydrogen pipelines, to 2 In 050, China is expected to build a large-scale green hydrogen network, meet most of the demand with local supply, and achieve self-sufficiency.

The development of China’s hydrogen energy ecosystem presents opportunities for multiple industry players. Since 2018, top domestic oil and gas companies have been actively participating in the pilot construction of hydrogen refueling stations using their expertise in the gas station network and perfect infrastructure, and coal chemical companies are also joining the ranks of hydrogen production and infrastructure construction. At the same time, new players in the hydrogen energy market are emerging one after another. For example, many car companies have started to develop hydrogen fuel cell vehicles (FCEVs), and are expected to invest in the construction of self-operated hydrogen production plants and hydrogenation facilities in the future. In addition, from a value chain perspective, full-service hydrogen service operators are also likely to emerge. Different stakeholders (e.g. governments, utilities, etc.) will be involved to maximize value through integrated services (e.g. end-to-end solutions, green hydrogen project validation, etc.). All of these developments can bring investors a variety of potential investment opportunities.

02 Green Transportation

Green transportation and low-carbon travel have undoubtedly become the most popular investment themes. As far as the Chinese market is concerned, most of the venture investments related to carbon reduction in recent years have been concentrated in the field of low-carbon travel. At the same time, with the promotion of regulatory policies and the improvement of consumers' awareness of low-carbon travel, there is still a lot of room for growth in the field of transportation upgrades.

We predict that by 2030, green transportation will bring investment opportunities of 2.3 trillion to 2.7 trillion US dollars, including electric vehicles, charging infrastructure, and next-generation battery technology, which are all potential investment directions.

Electric vehicles have the potential to become one of the biggest race tracks in green transportation. First, market demand is growing. We predict that by 2025, the penetration rate of pure electric vehicles in light vehicle sales will increase to 14%~16% of the total global sales; while the penetration rate in truck sales is expected to increase to 30%~55%. Secondly, in terms of cost, the total cost of ownership of electric passenger cars and light commercial vehicles is currently comparable to that of internal combustion engine vehicles, and the total cost of ownership of electric passenger vehicles will continue to decline as battery costs continue to decrease, which is expected to further increase Electric vehicle sales.

With the rapid development of the electric vehicle industry, its related supporting industries have also ushered in rapid growth, especially the charging infrastructure and the R&D and manufacturing of next-generation battery technology, which have brought attractive investment opportunities. Regulatory policies successively introduced under the goal of "carbon neutrality" have strongly promoted the development of domestic charging infrastructure. For example, in January this year, the National Development and Reform Commission and other departments issued the "Implementation Opinions on Further Improving the Service Support Capability of Electric Vehicle Charging Infrastructure", which proposed that by the end of the "14th Five-Year Plan", my country's charging infrastructure system can meet the needs of more than 20 million electric vehicles. charging needs. The substantial growth of the domestic charging infrastructure market has also attracted various investors to enter the market. For example, a leading Internet financial group in China invested tens of millions of yuan in a charging pile operation start-up company and became its second largest shareholder.

As the core link of electric vehicles, the development trend of battery manufacturing has also attracted the attention of all parties. For example, a domestic lithium battery company received an angel round of investment in the year following its establishment. Since its establishment 10 years ago, the company has continued to invest in research and development related to lithium batteries. Although there were no specific products on the market at that time, it was still favored by many upstream and downstream leading enterprises. The company successfully listed on the New York Stock Exchange in 2022, with a market value of more than billions of dollars.

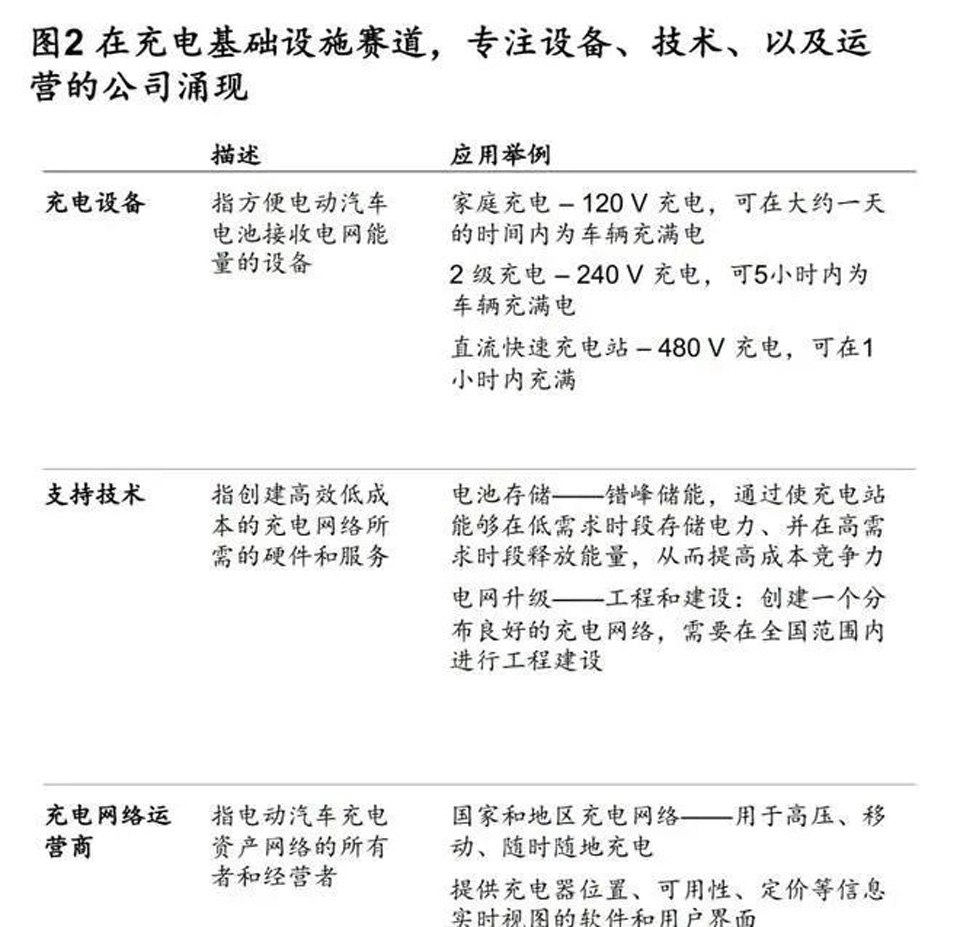

Track Digging - Charging Infrastructure

We predict that by 2030, the global sales of new energy vehicles will reach 70 million, of which 70% will be concentrated in China. At the same time, domestic demand for charging facilities and manufacturing technology are also improving simultaneously. Since Shenzhen began to build the first batch of electric vehicle charging piles in China in 2006, the construction and development of China's charging infrastructure has been mainly undertaken by the State Grid for many years, and has not been opened to social capital. Since then, as the country opened up the market for distributed power grid-connected projects and electric vehicle charging and swapping facilities, a large amount of private capital began to pour in. In 2020, charging piles will be included in the "new infrastructure", indicating that local governments will be inclined to the construction of charging infrastructure in terms of policy measures.

Many companies have begun to deploy in the field of charging infrastructure, focusing on the three major directions of charging equipment production, supporting technology development and facility operation (see Figure 2). For example, a domestic charging pile start-up company won the B round of financing from a number of leading investment companies in 2021, with a post-investment valuation of 15.5 billion. By integrating the small and medium-sized charging pile operating groups across the country, the start-up company provides Internet platform services such as unified payment, transaction management, operation and maintenance, and value-added services. Now it has formed a business model of "hardware + software + service", which ranks among the top in the country. Charging pile operator.

However, the charging industry still faces multiple challenges, particularly in terms of grid capacity and lack of interoperability between platforms, which companies are also grappling with. At the beginning of 2022, a domestic high-profile energy Internet of Things company was favored by leading investment companies. Coupled with the previous institutional investment, the company has completed hundreds of millions of US dollars in Series E financing. The energy IoT company improves the operational efficiency and energy supply efficiency of charging piles through algorithms and centralized supply, and realizes interconnection through digitalization, breaking the gap between charging equipment of different brands and platforms, and making the use of new energy more convenient. For example, in Shanghai, the company has intensively deployed cooperative charging piles, so that new energy vehicle owners can enjoy charging services at all cooperative charging piles just by scanning the code with one click.