Are electric vehicles more intelligent than fuel vehicles? The more expensive car has a higher intelligent configuration? Is Tesla's intelligence leading the industry? This may not be the case in reality.

Text | Zuo Maoxuan

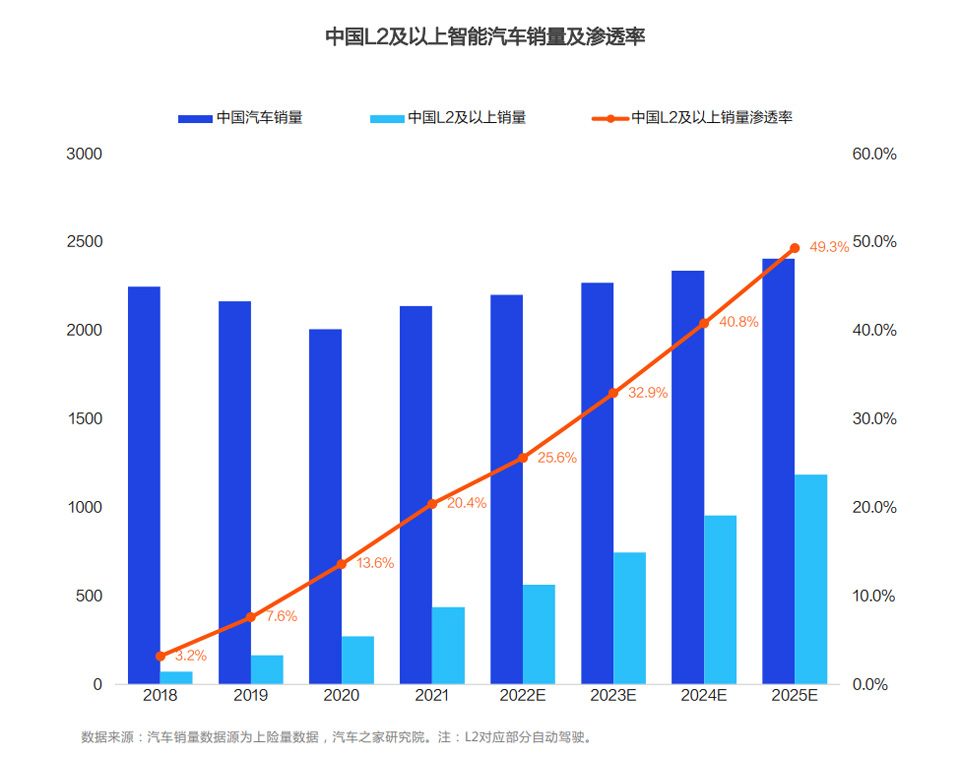

By 2025, China's L2 and above smart car sales will exceed 10 million units, and China's policy will shift from setting goals to guiding implementation and infrastructure construction.

The hardware configuration of the new forces is ahead of time, and the competition pressure of algorithm optimization and iteration is great.

The OTA upgrade penetration rate of million-dollar luxury cars is far less than that of ordinary family cars. China's new power brands especially prefer the facial recognition function, and intelligent feature configuration will become a new weapon for Chinese brands to compete in the differentiated market.

In terms of intelligent configuration, Tesla, the benchmark for autonomous driving, is inferior to Chinese brand models. The parking scene is unique to Chinese brands, but the safe driving scene needs to be improved urgently.

In 2007, Steve Jobs released the first generation of iPhone, "Apple" redefines the mobile phone. In the past 15 years, smartphones have profoundly changed people's lives as a carrier of innovation.

Now, as the automotive industry transforms, software-defined cars change the attributes of cars. There is no doubt that smart cars will be a huge innovation carrier in the future, not only with broad business prospects, but also redefining mobility and lifestyle.

In recent years, new car manufacturers such as Tesla, NIO, and Xiaopeng have been sought after by consumers and investors. More and more technology companies such as Baidu, Huawei, and Xiaomi have entered the automotive industry, trying to subvert the value chain of the automotive industry. and ecological structure.

However, there are still a series of contradictions and controversies about the development path of smart cars. Should enterprises focus on bicycle intelligence or vehicle-road collaboration? What core technologies should car companies have, and which technologies can be realized through external cooperation? What features should smart cars have today, and which ones aren't that useful?

All industry players need to answer the question: what kind of smart cars does the market need?

High-level autonomous driving technology is still a castle in the air. In the process of gradual development, it is not only necessary to have a clear judgment on the overall development trend of the smart car industry, but also to explore the real needs of consumers to explore future product development trends.

In the perception of some people, electric vehicles are more intelligent than fuel vehicles, and the more expensive vehicles seem to have higher intelligent configurations, and Tesla's intelligence is leading the industry. However, this may not be the case in reality.

In order to integrate and strengthen resources, and expand and strengthen its professionalism and influence in the entire automotive industry, 21st Century Business Herald established the 21st Century New Automobile Research Institute in November 2021, focusing on new trends in the development of automobiles in the era of smart electric vehicles, Research on major topics such as the reshaping of the entire automobile industry chain from the production end to the consumer end; as the industry's leading media, Autohome officially established the Autohome Research Institute in March this year, aiming to create a foresight of the auto industry It is a research think tank that uses industry advantages to provide perspectives on a series of important issues in the development of China's auto industry.

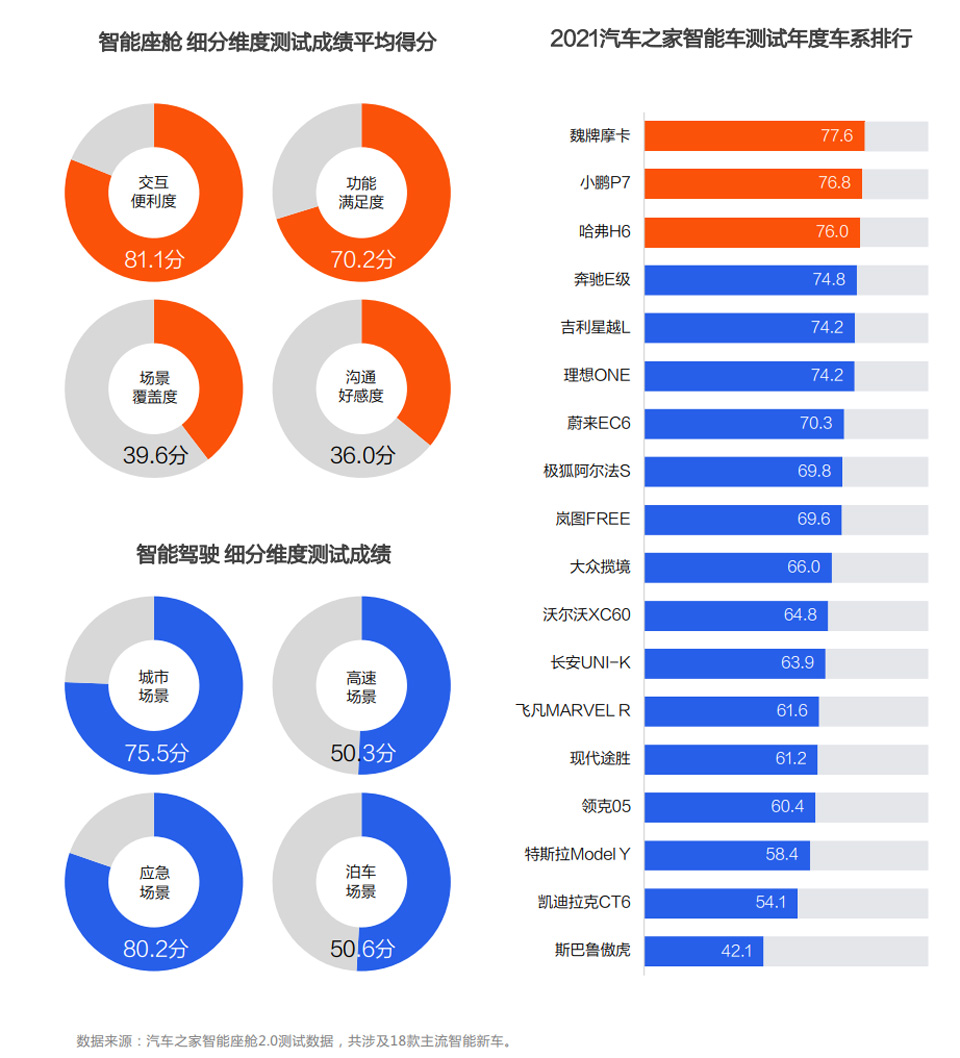

On April 27, the "2022 China Smart Vehicle Development Trend Insight Report" (hereinafter referred to as the "Report") jointly released by the Autohome Research Institute and the 21st Century New Automobile Research Institute shows that the Chinese brand model iV-RATING (Intelligent Vehicle Evaluation System) ) test scores are eye-catching. Among the 18 mainstream smart cars participating in the test, the Tesla Model Y ranks third from the bottom.

It should be pointed out that the average total score of the 18 mainstream smart cars participating in the test is only 66.4 points, and there is still a lot of room for improvement in smart cars. Each car company has different advantages, but their shortcomings are also very obvious.

China's L2 and above smart car sales will exceed 10 million in 2025

The automobile intelligent revolution is an important opportunity for my country's automobile industry to change lanes and overtake. In the past few years, relevant government departments in my country have successively issued a series of industrial policies to promote the rapid development of my country's smart car industry.

It should be pointed out that, after years of development, the policy has gradually shifted from the original setting of goals and specification to guiding implementation, building infrastructure, and network and data security.

Judging from the overall development trend of smart cars, the main areas of innovation include smart cockpit and smart driving.

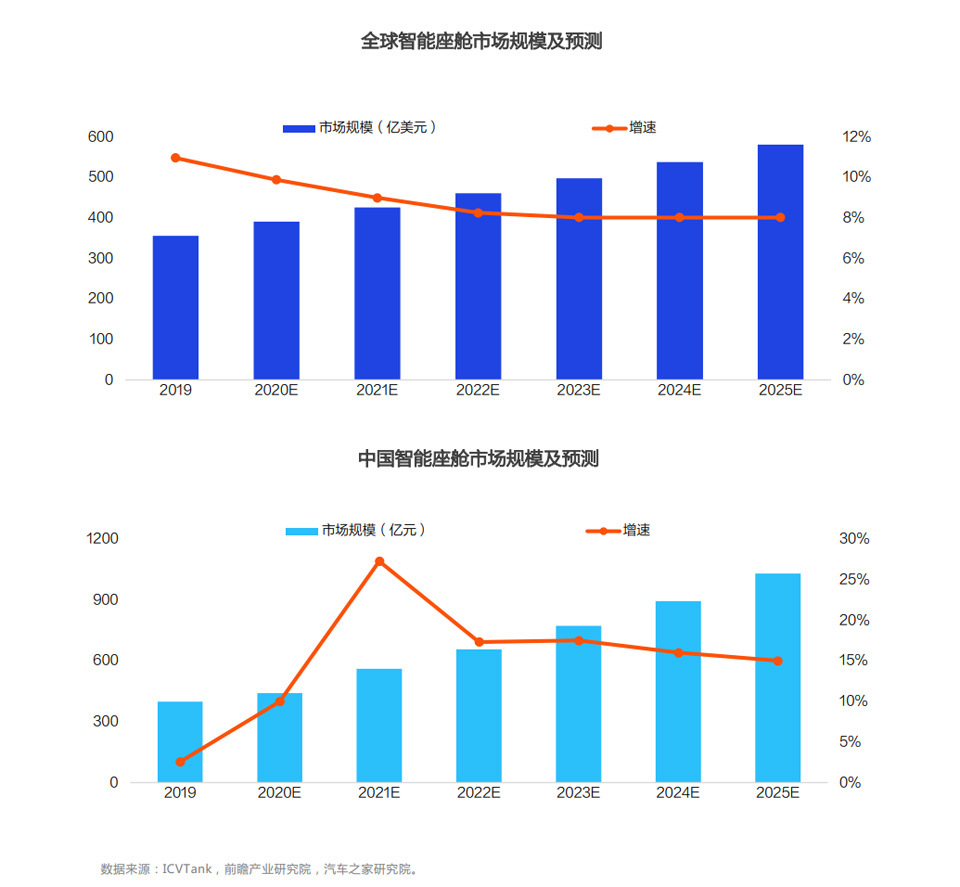

As the car becomes the third space of life, the popularity of smart cockpits is accelerating. According to ICVTank data, the market size of the global smart cockpit industry is expected to reach US$46.1 billion in 2022. Among them, China, as the world's most potential automotive market, the smart cockpit market in 2019 reached 44.1 billion yuan, and it is expected to reach 103 billion yuan in 2025.

At present, mainstream car companies are increasingly using chips from consumer electronics manufacturers such as Qualcomm, Nvidia, Intel, and Huawei. The chips are smaller in size and lower in heat, with higher computing power, and better guarantees for stability and speed.

In terms of central control screen and instrument panel, the trend of large-screen IVI led by Tesla is obvious. Touch large-screen IVI and one-core multi-screen IVI will become the mainstream. Many car companies have enlarged the size of the central control screen to enhance the sense of technology. , enhance the user experience with touch and voice.

On the whole, smart cockpit is the main breakthrough for many car companies to improve user experience because it is easier to be perceived by users and the technology is less difficult to develop than smart driving. The owner's life ecology is opened up.

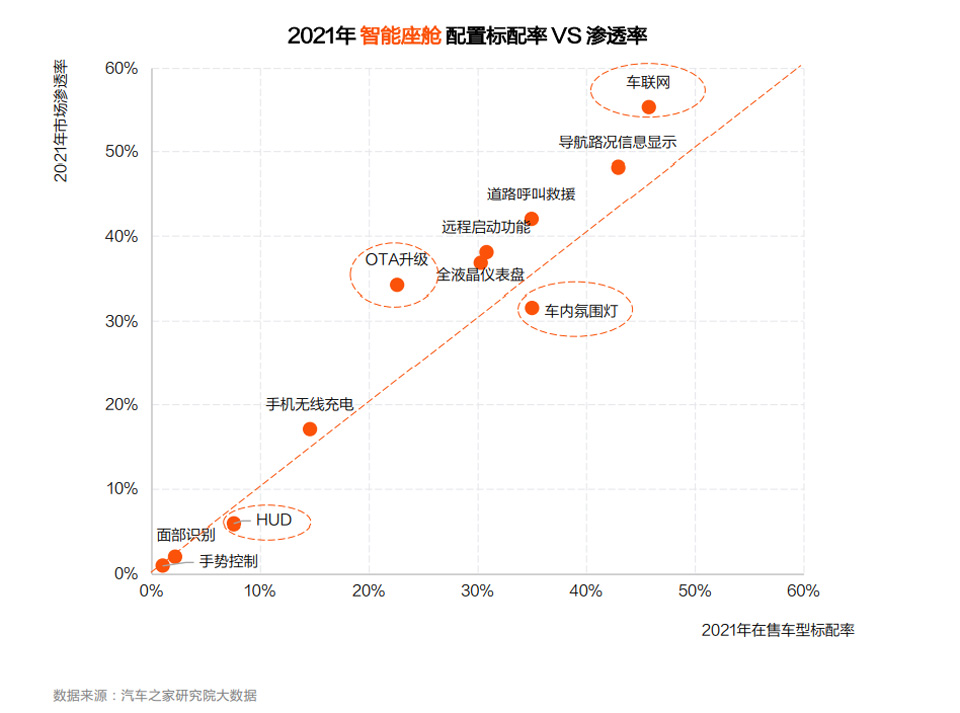

In addition, the market penetration rate of network connection function configuration is rapidly increasing, with a 5-year average compound growth rate of nearly 60%, especially the OTA upgrade, the 5-year compound growth rate is as high as 122.7%. In the future, rapid iterative updates will become the basic equipment of smart cars.

At the same time, with the development of 5G and Internet of Vehicles technologies, new human-computer interaction experiences are being combined with more scenarios to achieve richer forms of interaction. For example, by 2021, the penetration rate of wireless charging of mobile phones has reached 17.1%, an increase of 9.7 times compared with 2017, and the 5-year compound growth rate of gesture control is as high as 136.6%.

In the field of intelligent driving, L2-level autonomous vehicles are in the stage of commercialization and development.

There are two main paths for car companies to deploy intelligent driving. One is a full-stack word model represented by new cars such as Tesla, NIO and Xiaopeng, and the other is car companies, technology companies and autonomous driving startups. deep cooperation.

However, the "Report" believes that many of the current cooperation is to complete the optimization of algorithms and the integration of software and hardware. As competition continues to intensify and the pace of financing slows down, car companies are likely to make up for their shortcomings in the field of autonomous driving through mergers and acquisitions.

According to the data of the "Report", as the cost of key parts and components will continue to decline, the superimposed industrial environment will mature and technology will continue to progress. %.

The "Report" shows that the market penetration rate of L2-class models has grown rapidly in the past five years, an increase of 24.5 times compared with 2017. As the price of autonomous driving hardware continues to drop, the L2-level configuration penetrates down to the market segment in the low price range. By 2021, models in the range of 200,000 to 300,000 have rushed into the first camp, with a penetration rate of 37.6%.

At present, the overall penetration rate of autonomous driving of new energy vehicles is higher than that of traditional fuel vehicles. By 2021, the market penetration rate of L2 autonomous driving of new energy vehicles will reach 33.7%, much higher than the 19.0% of non-new energy vehicles.

It should be pointed out that in the past two years, in the field of autonomous driving, there has been a fierce "arms race" in areas such as the number of sensors, lidar applications, and chip computing power.

Judging from the configuration of the car series planned or launched in 2022, the new power car companies have advanced hardware configuration, which can basically meet the upgrade of autonomous driving services for car owners at this stage in a few years.

For example, the computing power of Xiaopeng G9 has increased from 30TOPS of Xiaopeng P5 to 508TOPS; the computing power of NIO ET7/ET5 is the highest, reaching 1016TOPS; Ideal has increased from 10TOPS of Ideal ONE to 508TOPS of L9.

Of course, the pros and cons of autonomous driving are not simply based on the computing power of the chip, but also require car companies to continuously optimize perception algorithms, planning algorithms, control algorithms, etc. It is necessary to integrate the execution layer and the interconnection layer to achieve higher-level autonomous driving, which will become the key to whether the intelligent driving service can be recognized by users in the future.

In addition, intelligent features such as facial recognition and gesture control are the product selling points of differentiated competition among brands. Chinese brands started earlier and developed more rapidly in this regard. The differentiated advantages of these emerging configurations may become new weapons for Chinese brands to compete in the market.

In addition, OTA upgrade capability is also an important factor to measure the intelligence level of enterprises. Chinese car companies are also at the forefront of the world in this field. The OTA upgrade penetration rate of Chinese brands is much higher than that of overseas brands.

Although the penetration rate has shown a trend of rapid increase since 2020, the market penetration rate of models with more than 1 million vehicles is still the lowest compared with other market segments. Mainly due to the fact that most of the models with a guide price of more than one million belong to ultra-luxury brands. Or sports car brands, and OTA upgrade is not just a simple configuration, but more of the operating cost behind it. Therefore, for ultra-luxury brands, there is no high necessity at the moment.

Tesla's intelligent comprehensive ability ranks last

With changes in consumption trends, intelligent capabilities have become an important factor in consumers' purchase of automobiles. However, consumers often understand the intelligence level of various car companies through the publicity of car companies or short-term test drives, and they cannot fully judge the merits.

Measuring the intelligence level of a smart car and a car company requires comprehensive consideration of the comprehensive capabilities of all aspects, as well as an authoritative and fair evaluation system. It is understood that the Autohome iV-RATING smart car evaluation system includes 2 categories of smart cockpit and smart driving, and a total of 8 professional tests on the dimension of real user scenarios. The test strictly follows 36 strict standards and 75 subdivision evaluation standards.

According to the iV-RATING smart car evaluation system, as of 2021, the average total score of the 18 mainstream smart cars participating in the test is only 66.4. In terms of products, smart cars still have a lot of room for improvement.

The results show that the advantages and disadvantages of each model are obvious, and both the intelligent cockpit and intelligent driving have the disadvantages of uneven development. The main shortcomings of smart cockpits lie in scene coverage and communication favorability; the main shortcomings of intelligent driving lie in high-speed and parking scenarios.

On the whole, the performance of Chinese brand car series is more eye-catching. The top 3 in the total score are all Chinese brand enterprises. There are 8 Chinese cars in the top 10 models, and the special The Tesla Model Y is only 16th out of 18 models.

In each subdivision dimension of the smart cockpit, different Chinese brand cars show their advantages in different fields and have their own characteristics. The highest score for interaction convenience is Xiaopeng P7; the highest score for functional satisfaction is Ideal ONE; the highest score for scene coverage is Geely Xingyue L, and the highest score for communication favorability is NIO EC6.

In terms of intelligent driving, Tesla, the autopilot benchmark in the traditional impression, is inferior to Chinese brands and only ranks eighth. Among the top 10 ratings, except for the Mercedes-Benz E-Class, which ranked 3rd, and the Tesla Model Y, which ranked 8th, all the others were Chinese brand models.

It is worth mentioning that Chinese brands have obvious advantages in the parking scene, but the scenes related to safe driving need to be improved urgently.

Among them, the parking safety scene, the dummy test scene, and the braking stability scene all have obvious shortcomings, especially the braking stability test. Safety is better than everything. Only on the basis of ensuring safety can it win the recognition of more consumers.

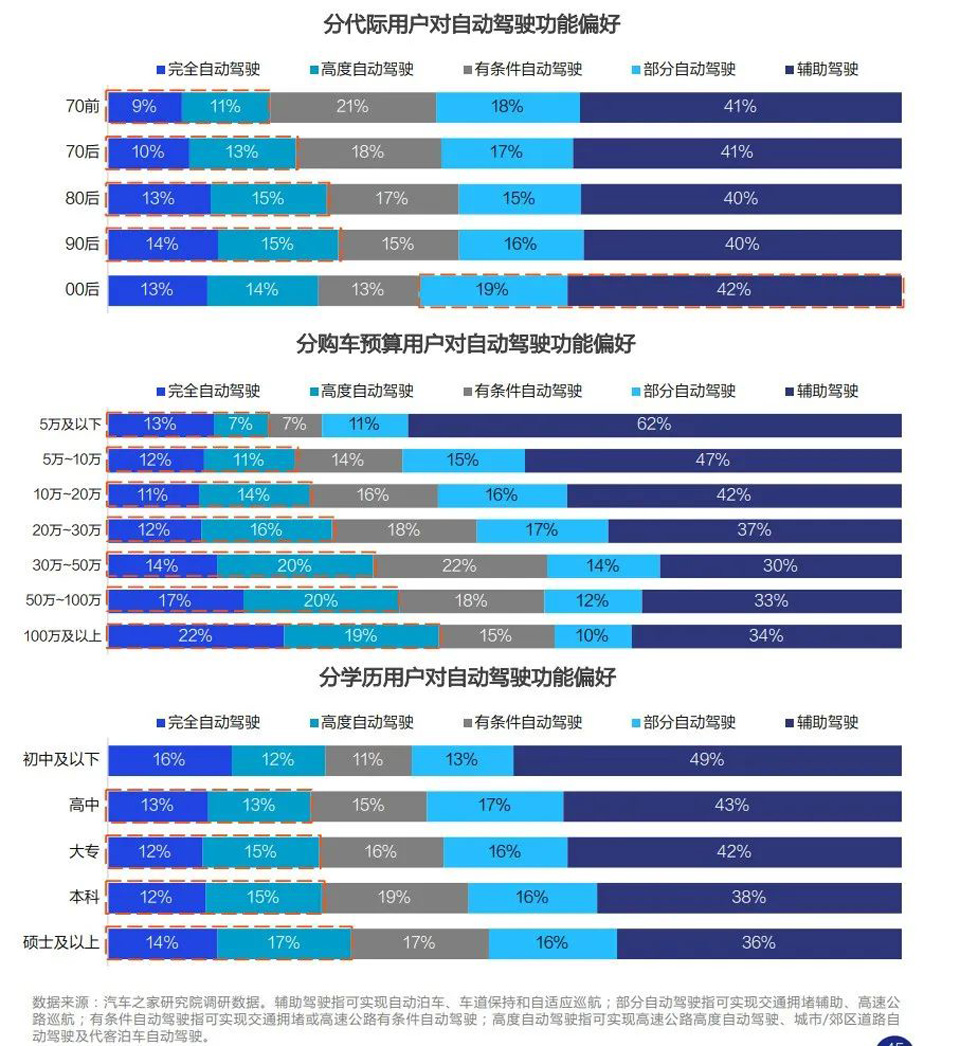

At present, more consumers are more willing to accept assisted driving, and only a few consumers prefer fully autonomous driving and advanced autonomous driving. From the perspective of the sub-groups of each generation, the acceptance bias trend is relatively similar. Although the young post-90s and post-00s users are more willing to accept fully autonomous driving and advanced autonomous driving, the proportion is not more than 30%.

Most consumers are already willing to pay for self-driving features. However, most consumers prefer the payment method to be "one-time purchase, low initial cost and additional fees for upgrades", and only a few consumers are willing to accept "pay by time or mileage".

In terms of traditional intelligent car configuration functions, the new generation group does not pay. From a generational perspective, people's preferences for the first six configurations of traditional cars are similar, but the post-00s generation is not very enthusiastic about them. Active braking/active safety system and full-speed adaptive cruise are the two configurations most valued by post-80s and post-90s, while the proportion of post-00s choosing them is much lower.

For configurations such as active braking, full-speed adaptive cruise, lane-merging assist, and lane departure warning systems, older users generally have higher acceptance.

In terms of preferences for emerging smart configurations, overall users have the highest preference for remote control of vehicles with mobile apps, A-pillar/chassis perspective imaging systems, and AR real-world map navigation configurations. The older users have a stronger preference for emerging vehicle configurations. After 00, the acceptance of emerging car configuration is relatively low.

Car companies battle smart cars in the second half

The "Report" found that at present, in terms of smart cockpit configuration, most of the configuration items are more demand than supply, which reflects that users are willing to pay more car purchase costs to buy higher-equipped models, especially for 300,000-500,000 models, which need to be improved in network configuration. Standard rate; gesture control and facial recognition are in a state of balance between standard rate and penetration, but the values are relatively low. In-car ambient lights and HUD users are slightly dissatisfied; the Internet of Vehicles and OTA upgrades are more popular in the market.

Therefore, in the various segments of the smart cockpit, the "Report" suggests that users of more than 150,000 models have strong demand for the Internet of Vehicles, and models with a guide price of 300,000 to 1 million need to further increase the standard rate, which will effectively improve users' awareness of the models. Satisfaction and purchase desire; for models with a guide price of 50,000 to 150,000, the standard OTA upgrade will be conducive to market competition. In addition, the price range that most needs to improve the standard rate is 300,000-1,000,000; 100,000-200,000, 100 Intentional users of more than 10,000 models are more accepting of the configuration and can strengthen publicity efforts; the actual market penetration rate of 50,000-150,000 and 200,000-300,000 models is lower than the standard rate, it is recommended to consider changing the standard to optional, and continue to observe Market feedback changes.

In terms of smart driving, judging from the comparison of the standard rate and market penetration rate of smart driving configurations in the sales car series in 2021, L2-level assisted driving-related configurations and safety configurations are particularly popular among consumers. However, the market situation of satellite navigation system, 360 panoramic image, parallel auxiliary and automatic parking is in the market situation of oversupply.

Specifically, although the configuration rate of 360 panoramic images of 100,000-200,000 models is relatively high, users will still give up the choice based on the cost of car purchase. They can consider switching to optional configuration, or try to change to the way of hardware pre-embedded paid subscription. ; Pre-order users of 200,000-300,000 models are more interested in active braking, and can consider increasing the standard rate; as one of the core basic configurations of L2 autonomous driving, pre-order users of 200,000-300,000 and 1 million or more models are more willing to Lane Keep Assist pays the bill. Users of 100,000-200,000 models are more willing to choose, and they can try to increase the standard rate on the premise of a slight increase in car prices, which is more conducive to market competition.

"Electrification is the first half, and intelligence is the second half." It is foreseeable that smart cars will be the most commercially promising field in the automotive industry in the future, but the competition will also be more intense.

For Chinese car companies, the development of smart cars presents both opportunities and challenges.

Based on the status quo and development trend of the smart car industry, the Autohome Research Institute and the 21st Century New Automobile Research Institute put forward six suggestions to Chinese automakers.

1. OTA should not be reduced to a tool for marketing or patching, and the host manufacturer should take back the initiative as soon as possible; 2. In the early stage of autonomous driving development, safety assurance should be the primary consideration; However, full-stack self-research must be the ultimate attribution; 4. Open source, open source, innovative breakthroughs, and establish systematic and powerful software capabilities; 5. AEB and mobile phone remote control vehicles have the highest willingness to pay, and can give priority to trial software subscriptions; 6. Improve the acceptance of smart driving users through smart driving activities, achievement exposure, and early adopters of functions.